Making Tax Digital is now live for landlords over £50,000. The £30,000 threshold lands April 2027.

Landlords with gross qualifying income over £50,000 in 2024/25 should already be filing quarterly. The £30,000 cohort is next, and the income year HMRC is testing is the one that just ended.

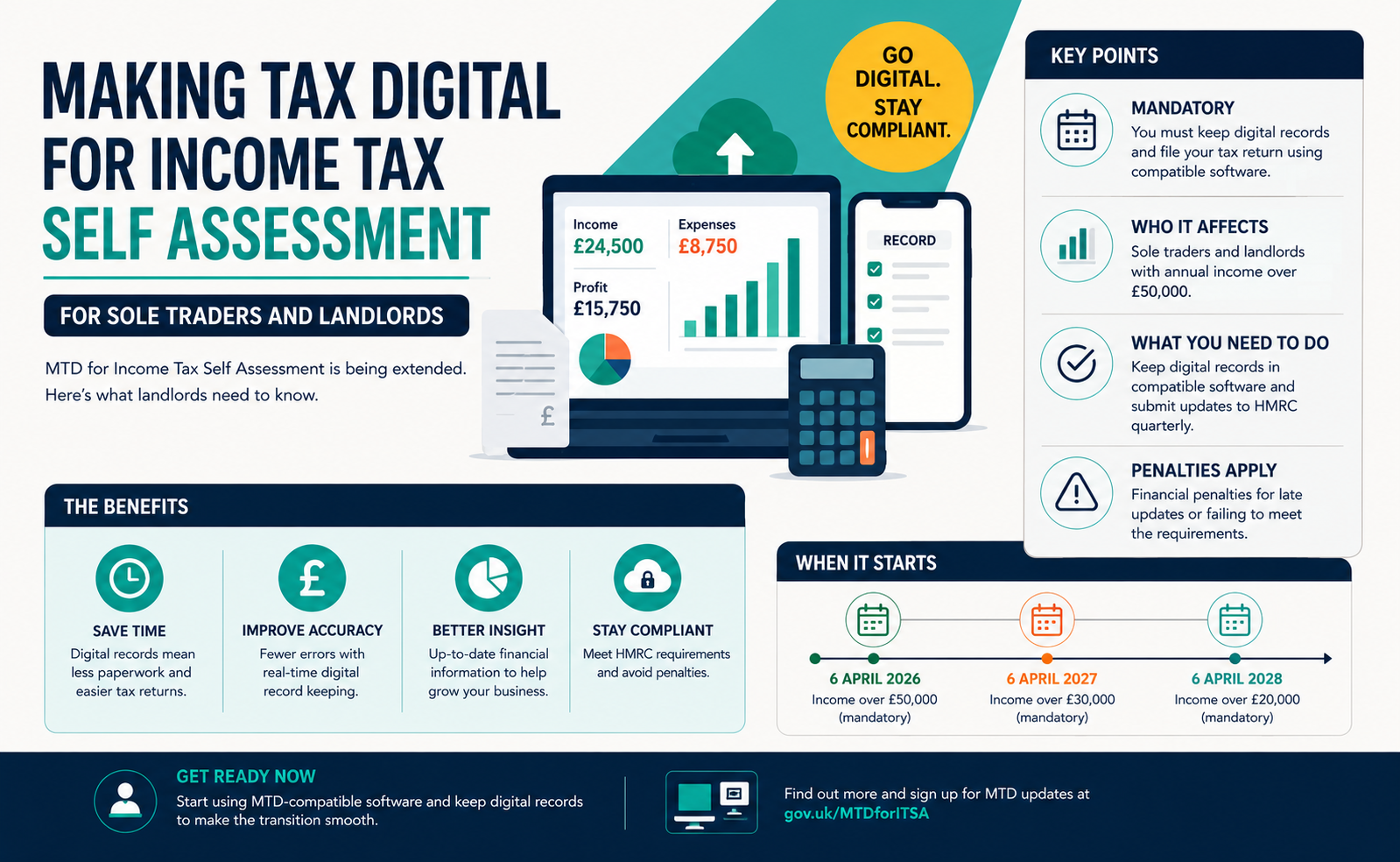

Making Tax Digital for Income Tax Self Assessment (MTD for ITSA) — the regime that has applied to VAT-registered businesses since 2019 — extended to sole traders and landlords on 6 April 2026. From that date, anyone with qualifying income above £50,000 must keep digital records, submit a quarterly update to HMRC, and finalise their year-end return through MTD-compatible software. The threshold drops to £30,000 from 6 April 2027 and £20,000 from 6 April 2028.

For landlords this is the biggest change to Self Assessment in three decades. ITSA hasn’t been a quarterly process since paper assessments — you’ve always had until 31 January after the tax year to pull your figures together. From now on, in-scope landlords file five times a year: four quarterly updates plus a final declaration. HMRC’s impact assessment estimates around 780,000 people are caught by the first phase, with another 970,000 to follow in 2027.

What counts toward the threshold

This is where most landlords misread the rule. “Qualifying income” is gross income from property and self-employment, combined, before any expenses. It is not your total taxable income — employment income, dividends, savings interest, and pension drawdowns are all outside the scope.

Some realistic examples:

- Three flats grossing £1,500 a month each = £54,000/yr → caught by the £50,000 threshold.

- One flat at £1,500/month + a freelance side gig grossing £15,000 = £33,000/yr → caught by the £30,000 threshold from April 2027.

- A jointly-owned BTL grossing £24,000 counts as £12,000 to each of two co-owners → under all current thresholds.

- One BTL grossing £1,800/month = £21,600/yr → caught by the £20,000 threshold from April 2028.

A few rules that routinely catch landlords out:

- Joint owners count only their share of the rent toward their personal threshold — the property doesn’t count once; it counts per-owner.

- Multiple UK rental properties are reported as a single “UK property business” for tax. You don’t file four sets of digital records for four flats; you file one rolling property P&L.

- Overseas property is a separate property business and counts separately in the qualifying-income calculation.

- Furnished holiday lets lost their special tax regime in April 2025; they now sit inside the standard property business and count toward the same totals.

The income year HMRC tests against differs by cohort, and this is the part that catches landlords cold:

- £50,000 mandate (live now): HMRC tested the 2024/25 Self Assessment return (filed by 31 January 2026). If you crossed £50k in 2024/25 you should already have an MTD start letter.

- £30,000 mandate (April 2027): HMRC will test the 2025/26 return — the tax year that just ended on 5 April 2026, due by 31 January 2027.

- £20,000 mandate (April 2028): HMRC will test the 2026/27 return — the tax year that started a month ago.

If your numbers are anywhere near a threshold, the 2025/26 return you’re about to file is the one that decides your April 2027 status, and the records you start keeping today decide your April 2028 status.

What you have to do

- Pull last year’s figures now. Add up your gross rent received between 6 April 2025 and 5 April 2026. Add any self-employment turnover. If the total is over £30,000 you’ll be mandated from April 2027 — you have eleven months to prepare.

- Move to digital records this tax year, ahead of mandation. Whatever method you use today (shoebox, spreadsheet, paper ledger), get to MTD-compatible bookkeeping software well before your start date. The transition is materially easier when you’re not also under deadline pressure.

- Pick software during the public beta. HMRC publishes a list of MTD-compatible products. Several offer free tiers for simpler landlord cases. Don’t lock in a paid annual contract until you’ve used the product through one or two beta quarters.

- Talk to your accountant early. Many are repricing for quarterly work, and most will want clients on a shared platform (Xero, FreeAgent, QuickBooks). If you wait until 2027 to have this conversation, your options narrow and the prices firm up.

- Apply for an exemption if you genuinely cannot go digital. The MTD for ITSA exemption process mirrors the one in place for MTD for VAT. The bar is high — “I don’t like computers” doesn’t clear it — but genuine digital exclusion does, and it can be applied for by phone or in writing.

Quarterly update dates

The standard tax-year quarters and their submission deadlines:

| Quarter covers | Update due |

|---|---|

| 6 April — 5 July | 5 August |

| 6 July — 5 October | 5 November |

| 6 October — 5 January | 5 February |

| 6 January — 5 April | 5 May |

Quarterly updates are cumulative — each one carries totals from 6 April to the end of the relevant quarter, not just that quarter’s activity. Errors get corrected in the next update; you don’t amend earlier ones.

The annual Final Declaration (which replaces the SA100 and SA105 paper return) is due by 31 January following the tax year, the same as today.

Where the risk actually lives

The headline numbers in HMRC’s impact assessment are the costs: around £320 transitional and £110 annually per business. For most landlords those figures are unrealistically low — they don’t account for accountant repricing, the time cost of keeping books quarterly rather than annually, or the practical reality that “compatible software” usually means subscribing to a bookkeeping platform you didn’t previously need.

Two specific risks for landlords:

- The threshold-cliff effect. A landlord whose gross rent crosses £30,001 in 2025/26 is mandated from April 2027 onward, even if their taxable profit is near zero after mortgage interest, repairs, and agent fees. MTD doesn’t care about profit. If you’re close to a threshold, think about whether bringing forward expenses or holding back a rent review would defer the mandate by a tax year — and whether that’s actually worth the operational hassle.

- Penalty points stack quickly. Late updates fall under HMRC’s points-based regime. Quarterly filers hit the points threshold where fixed penalties begin much faster than annual filers do — the same number of misses bites sooner. Get the dates into your calendar before you need them.

The shift from one annual filing to five, all underpinned by software you may not currently use, takes preparation. Start the groundwork in the tax year before you’re mandated, not the one when you are.

Sources

- Making Tax Digital for Income Tax Self Assessment for sole traders and landlords — HMRC policy paper

- Find software that’s compatible with Making Tax Digital for Income Tax — gov.uk

- Income Tax (Digital Requirements) Regulations 2021 — legislation.gov.uk

This is general information, not tax advice. If you’re unsure how MTD applies to your specific situation, talk to your accountant or HMRC before acting.

Get briefings like this, monthly.

Landlord Brief is a short, plain-English digest of what's changing in UK rental law — with sources. One email on the 1st. Free.

Unsubscribe in one click from any email.